When people talk about blockchain, the first thing that comes to their minds is usually cryptocurrency. Bitcoin, Ethereum, and Dogecoin are household names nowadays. But, in truth, the technology behind blockchain is far more important than just digital coins. It is a trust infrastructure that underpins the entire digital world.

To illustrate, consider a scenario where you want to shop online. You make the payment, but does the seller believe that you have done so? The seller then ships you the goods, but do you trust that it is the right item that you have received? Right now, banks, PayPal, and Amazon are the ones who have created this trust, and they do it through their reliable middleman service.

What is Blockchain Technology?

The blockchain technology is an advanced database system that permits transparency in information dissemination across the enterprise network. A blockchain database keeps its information in blocks that are connected in a chain-like structure.

The data is in perfect chronological order because it is impossible to remove or change the chain without the agreement of the whole network.

Thus, one of the uses of blockchain technology is to build an unchangeable or immutable ledger for tracing orders, payments, accounts, and other transactions. The system incorporates features that block entry of unauthorized transactions and provide a consistent view of these transactions in the network at the same time.

How Blockchain Works: Step-by-Step Process

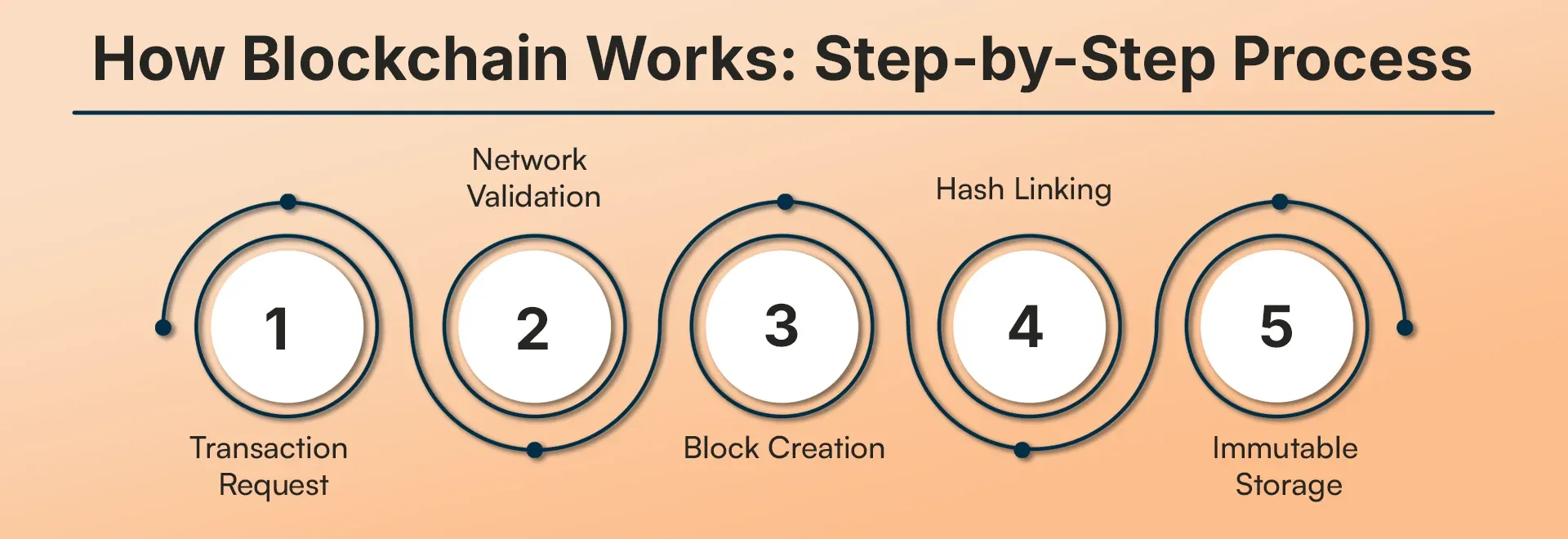

Let's consider a practical scenario. Raj aims to transfer funds via blockchain to Priya:

Step 1: Transaction Request: Raj starts the process by sending out a transaction: "I wish to transfer ₹5000 to Priya." Subsequently, this request is spread throughout the whole network.

Step 2: Network Validation: The networks thousands of nodes, composed of computers, carry out a validation process for the transaction. They inquire: "Is Raj's ₹5000 balance real? Is the transaction valid?" A consensus must be obtained from the majority of the nodes.

Step 3: Block Creation: The transactions that were authenticated are then compiled together, and a block is created. This block contains Raj and Priya's transaction, along with other transactions that were waiting.

Step 4: Hash Linking: A cryptographic hash is used to link the present block to the last one. This creates a chain, the term "blockchain."

Step 5: Immutable Storage: The chain, once formed, cannot be altered as long as the block is not removed from it. It's quite impractical for no one to be able to change it without the majority of the network's approval.

All of this happens in a matter of minutes, and there is no need for a bank or any intermediary.

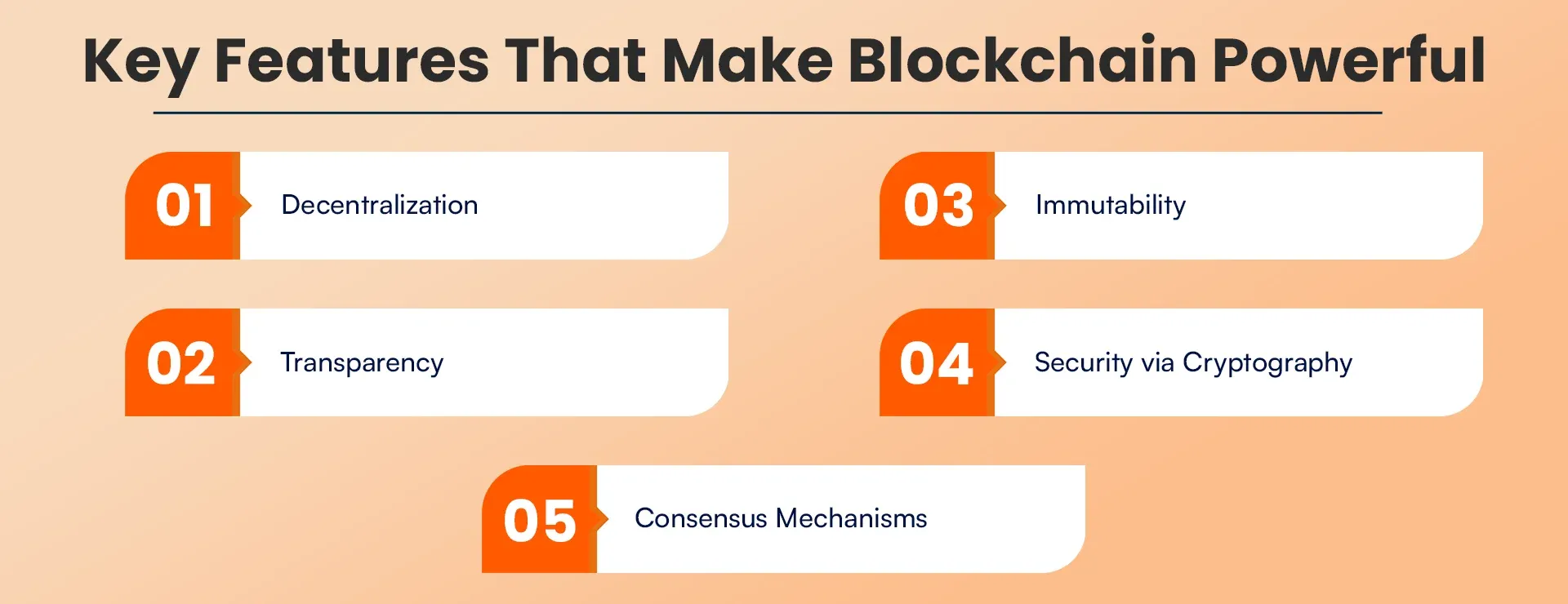

Key Features That Make Blockchain Powerful

-

Decentralization: No entity has complete control over it. The distribution of the network makes it possible to suffer from no single point of failure.

-

Transparency: The complete transaction history is open for the public to see (though the identities of the parties remain encrypted). Thus, anybody can check what has happened.

-

Immutability: Data once recorded on the blockchain is unalterable. This results in a record that is permanent and cannot be tampered with.

-

Security via Cryptography:hy Advanced encryption techniques ensure only authorized persons can access data. Private keys are like your passwords - lose them and you lose access.

-

Consensus Mechanisms Systems like Proof of Work (PoW) and Proof of Stake (PoS) ensure all nodes agree before a transaction becomes valid. This prevents fraud and double-spending.

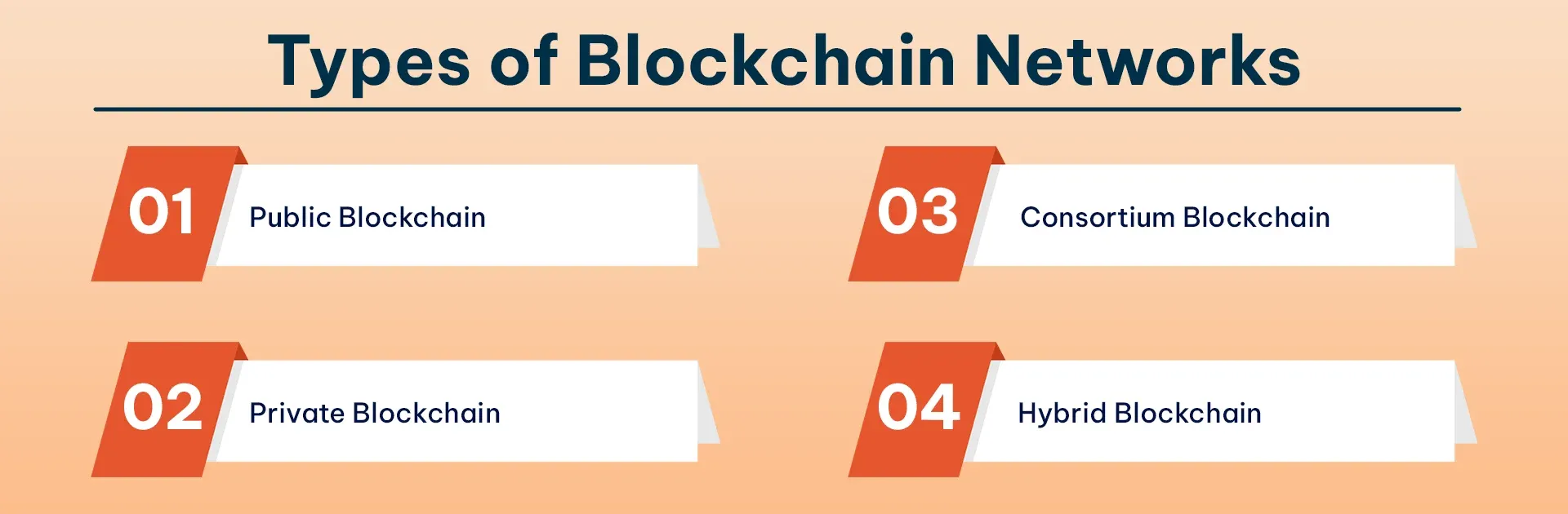

Types of Blockchain Networks

Some of the various types of Blockchain networks, which have been described below :

1. Public Blockchain

Public blockchains, such as Bitcoin and Ethereum, are available to anyone. Total transparency and openness are their characteristics. Nevertheless, they may be slow and consume a large amount of electricity.

2. Private Blockchain

Private blockchains are set up by companies for their internal use. They can only be accessed by authorized personnel. They are quicker and more efficient, but transparency is lower.

3. Consortium Blockchain

These are controlled by a number of organizations together. Such a set-up is used by banking consortia or networks in the supply chain. A hybrid approach to decentralization.

4. Hybrid Blockchain

It has the features of both public and private. Access control with a portion of transparency. It is the best solution as it combines the positive aspects of both worlds.

Blockchain: A Trust Layer, Not Just Technology

We've been examining the blockchain from the angle of technology. But the truth is, it is a trust base. Let me make it clear to you.

In ancient systems, trust was the major factor that affected the role of human intermediaries. This was how the whole thing went: banks believed both the customer and the seller, the judicial system gave power to trustworthy contracts, and the government granted certificates for trustworthy documents. All these were the "trust providers."

Blockchain creates trust in a way that is entirely based on mathematics and cryptography. The code behaves exactly like it is programmed to. Human bias is out of the equation; there is no corruption and no selective enforcement. This is what we call the "code is law" principle.

Now, what we talk about here is quite a different thing when it comes to trust in the digital world as compared to trust in the human one. Human trust is built on relationships, reputation, and legal systems, while digital trust rests on algorithms and cryptography. Neither system is without flaws; however, blockchain opens an unprecedented middle ground.

Hidden Costs Nobody Discusses

Blockchain has numerous pros, but at the same time, some expenses are not usually mentioned:

Energy Consumption Mining Bitcoin uses a lot of electricity and, hence, is a major energy consumer. Even though the systems using Proof of Stake have made this issue better, large networks are still consuming a considerable amount of energy.

On the one hand, immutability is an advantage, and on the other, it is a drawback too. Wrong data, sensitive information, or illegal content on the blockchain can never be deleted,d as it stays there forever.

Regulatory Uncertainty: Governments are still determining the best way to regulate blockchain. This ambiguity is a risk factor for businesses.

When Should You NOT Use Blockchain?

Blockchain will not solve all problems. Below is an uncomplicated checklist:

- A traditional database is the best option if you just want to keep simple data.

- If a single organization is in control of the whole process, there is no need for a blockchain.

- Is it a case that you will be constantly updating/deleting data? Not a good idea to use blockchain.

- If what you want is speed rather than immutability, then traditional systems are the right choice.

Trust, transparency, and immutability are the only factors in a cost-benefit analysis where blockchain is an advisable option.

Real-World Applications Beyond Crypto

-

Supply Chain Traceability

Walmart and IBM are utilizing blockchain technology for tracking food supply chains. The source can be pinpointed within minutes instead of days once contamination is found.

-

Healthcare Records

Patient archives can be securely shared among various medical institutions. It is the patients who determine who can access such data.

Digital Identity. If Aadhaar-like systems are established on blockchain, deceit and identity theft could be cut down significantly.

-

Smart Contracts

Auto agreements that take effect when terms are fulfilled. Claims and property transfers can be concluded without human intervention.

-

Voting Systems

Theoretically,y transparent and secure elections are possible;e, nevertheless, real-world applications still face difficulties.

Why Blockchain Projects Fail

Reality check: The majority of projects within the blockchain have to die. Some of the usual reasons for failure include:

Making overly complicated solutions for basic issues, not proper decentralization (the company still has power over everything), a horrible user experience, a lack of knowledge about regulations, and above all, attempting to solve problems that are not there.

The invisible side of successful blockchain projects. The users never notice that blockchain is in the backend. This delicate integration is actually an adoption.

The Future: Blockchain + AI Integration

The union of AI and blockchain is the next frontier. Think of a scenario where AI takes decisions, and blockchain authenticates and documents these decisions in an unchangeable manner. Contracts that are self-executing and based on AI signals. Companies that run entirely on machines with no human interaction.

In the long run, blockchain will be an infrastructure layer that users won't be aware of. Similar to internet protocols (TCP/IP) that you do not notice but that every website relies on, blockchain will also be such an invisible infrastructure.

Conclusion

Blockchain's major asset is its transparency, as itisy not seen. There is no direct interaction between the users and the blockchain. Yet in the long run, it has been building trust quietly, eliminating middlemen, and efficiently managing the transactions.

In the year 2026, blockchain has already cleared the hype cycle. The price speculation and drive for fast money have lessened. However, the very slow but real and practical use is still going on. Banks are relying on blockchain technology for international payments. Governments are looking into digital currency. Companies are blending it with the supply chains.

If your business is ready to move from experimentation to real implementation, RejoiceHub can help you design and deploy blockchain-powered solutions that align with your growth strategy securely, scalably, and with long-term impact in mind

Frequently Asked Questions

1. Is blockchain only used for cryptocurrency?

No, blockchain is used beyond cryptocurrency for supply chain tracking, healthcare records, digital identity, smart contracts, and secure data sharing between organizations.

2. What are the main features of blockchain technology?

The main features are decentralization, transparency, immutability, and consensus mechanisms that ensure data is secure, verified, and cannot be altered.

3. What is the difference between public and private blockchain?

A public blockchain is open to anyone and fully transparent, while a private blockchain is restricted to selected users and controlled by an organization for internal use.

4. What is a smart contract in blockchain?

A smart contract is a self-executing digital agreement that automatically runs when conditions are met, without needing lawyers or third parties.

5. Why is blockchain considered secure?

Blockchain is secure because data is encrypted, stored across many computers, and cannot be changed without approval from most of the network.

6. What are the disadvantages of blockchain?

Blockchain can consume high energy, face regulatory uncertainty, and makes it difficult to remove or correct data once it is recorded.

7. When should you not use blockchain?

You should not use blockchain if you only need a simple database, need fast updates, or if one organization controls the entire system.

8. How is blockchain used in real life?

Blockchain is used in food supply tracking, digital payments, healthcare data sharing, identity verification, and automated legal agreements.

9. What is the future of blockchain technology?

Blockchain’s future lies in becoming a hidden infrastructure for digital systems, working alongside AI to verify decisions, automate contracts, and secure global transactions.

10. Can blockchain work without the internet?

No, blockchain requires internet connectivity to share data between network nodes and maintain synchronization across the system.

11. Is blockchain legal in India?

Blockchain technology itself is legal in India, but regulations around cryptocurrencies and digital assets are still evolving.

12. How does blockchain create trust?

Blockchain creates trust by using mathematics and cryptography instead of human intermediaries, ensuring data is verified and cannot be manipulated.

13. What industries benefit the most from blockchain?

Industries like banking, healthcare, supply chain, government services, real estate, and cybersecurity benefit the most from blockchain technology.